Share this:

Google+

< Previous | Contents | Next >

How to forecast using Random Walk?

Example

Several years of data show that the demand is following a white noise. Suppose this year demand is 100 metric ton. What would be the prediction of demand in the next year and next two years?

Answer:

Using random walk, we have \( x_{t+1}= x_t + N(0,1) \). Since this year data is 100, then next year demand would be \( x_{1}= x_{0} + N(0,1) = 100 + N(0,1) = N(100,1) \). The second years demand would be \( x_{2}= x_{1} + N(0,1) = N(100,1) + N(0,1) = + N(100,\sqrt{2}) \). The summation of two independent normal distributions is $$ N(\mu_1,\sigma_1) + N(\mu_2,\sigma_2) N(\mu_1+\mu_2,\sqrt{\sigma_1^2+\sigma_2^2}) $$.

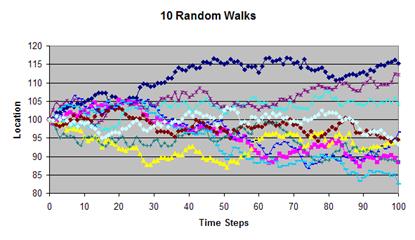

One weakness of naïve forecast based on random walk is that it is producing a range that easily goes beyond the range of the variable being forecast. Figure below shows 10 random walks starting from an initial location of 100. If we take the average of the 10 random walks below the results would be the same as the initial location. The random walk process has no trend. In general, if the process follows a Brownian motion, the predicted demand for \( t \) numbers of years would be $$ x_t=x_0 + t N(0,1) = x_0+ N(0,\sqrt{t}) = N(x_0,\sqrt{t}) $$.

< Previous | Contents | Next >

Do you have question regarding this Stochastic Process tutorial? Ask your question here

These tutorial is copyrighted .

Preferable reference for this tutorial is

Teknomo, Kardi. (2019) Stochastic Process Tutorial .

http://people.revoledu.com/kardi/tutorial/StochasticProcess/