Share this:

Google+

< Previous | Contents | Next >

Simulation of GBM in Excel

To simulate GBM in a spreadsheet, you need to create the simulation of Brownian motion first. Copy the sheet of Brownian motion and rename it as GBM.

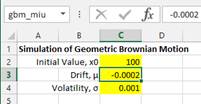

1.First, provide the values of three parameters and name them in the name box respectively as gbm_x0, gbm_miu and gbm_sigma.

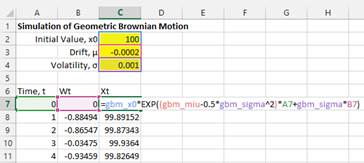

2.Then, compute Xt=x0*exp(μ-0.5*σ^2)*t+σ*wt). See the picture below for the actual implementation in spreadsheet

3.Copy the formula until certain time, say t=250

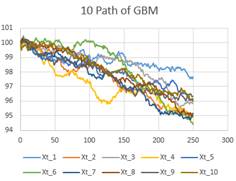

4.Plot the path of Geometric Brownian motion

< Previous | Contents | Next >

Do you have question regarding this Stochastic Process tutorial? Ask your question here

These tutorial is copyrighted .

Preferable reference for this tutorial is

Teknomo, Kardi. (2017) Stochastic Process Tutorial .

http://people.revoledu.com/kardi/tutorial/StochasticProcess/